Inflation and the corresponding rise, then fall, in interest rates have been on nearly every Canadian’s mind for years. Practically everywhere one looks, there has been talk about the far-reaching consequences of these important financial indicators, but how do these shifts affect landlords and real estate investors? Those who own rental properties have felt the impact of Canada’s changing interest rates in several important ways. We’re seeing rent prices adjust as landlords respond to shifting mortgage costs, vacancy rates, and other market pressures. Today, liv.rent will walk you through exactly what the current interest rate environment means for Canadian landlords, in terms of the overnight rate, mortgage rates, home sale prices, and more.

Note: This post has been updated to reflect the April 29, 2026 announcement from the Bank of Canada.

Is your rental priced competitively?

Find out with a free rent estimate. Our team of rental experts will calculate your unit’s true value based on your listing details & current market trends.

What is inflation?

Inflation has dominated economic conversations for several years now, but what does the word actually refer to, and what are its tangible effects? In the most basic terms, inflation refers to the gradual rise in the price of goods and services over time, or more specifically, the decrease in purchasing power of a currency. This is typically seen as an aggregate measure of the general cost of living, which results in a slowdown of economic growth since individuals have less money to spend on non-essential goods.

According to Statistics Canada, Canada’s inflation rate rose to 2.8% in April 2026, up from 2.4% in March, driven largely by energy price increases tied to geopolitical disruptions in the Middle East. For context, the Bank of Canada strives to maintain a 2% inflation rate each year as part of its mandate. In terms of real estate, inflation has some bearing on generally higher housing prices across the board, although it isn’t the only factor driving Canada’s housing costs.

What do interest rates represent?

The majority of Canadians are already familiar with interest rates in their daily lives, but it’s worth clarifying the key terms. Broadly speaking, interest rates are the amount that a lender charges a borrower over time, generally expressed as a percentage of the principal loan. On a federal scale, there are two primary interest rates that individuals, and homeowners in particular, should be aware of: the overnight rate and the prime rate. The former is set by the Bank of Canada itself, while individual banks determine their own prime rate.

Overnight rate

The overnight rate is set by Canada’s central bank and is an indicator of the rate each individual bank will set, since they need to cover this rate while still earning a profit overall. When the Bank of Canada raises the overnight rate, it becomes more expensive for banks to borrow money, and those costs get passed onto borrowers through higher prime rates.

Prime rate

The prime rate represents the base interest rate that a bank will lend money for in order to cover the overnight rate, as well as account for its own operating costs. This does not mean that this rate is the actual rate customers will be offered, since individual clients can receive discounts based on a variety of factors. As of May 2026, Canada’s major banks have a prime rate of 4.45%, unchanged since the Bank of Canada’s October 29, 2025 rate cut.

How interest rates relate to inflation

Interest rates are fundamentally tied to inflation since the former is one of the main methods used by central banks to manage the economy. Higher interest rates encourage saving while discouraging borrowing and spending, while lower interest rates are more amenable to higher levels of spending. In response to high interest rates, businesses will typically increase the price of their products more slowly, or even lower them to encourage more spending. Similar effects can be seen in the real estate market. High interest rates make qualifying for mortgages harder, lowering demand and gradually causing home prices to adjust.

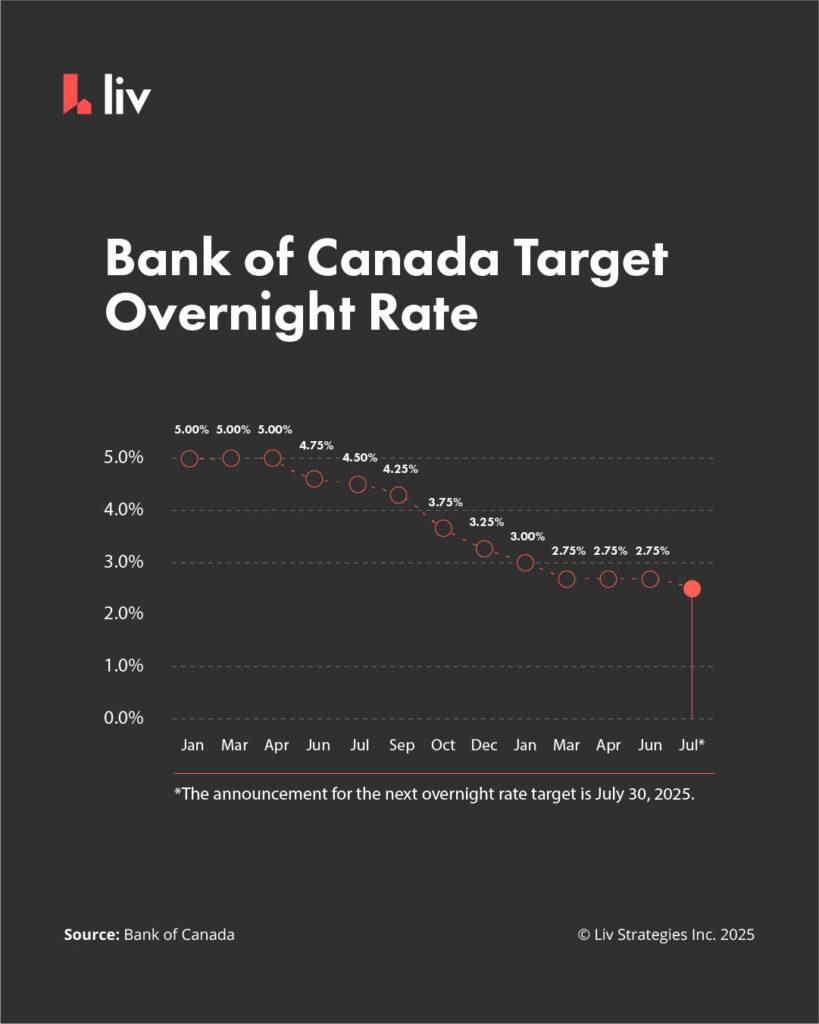

It makes sense that during periods of high inflation, central banks raise interest rates to lower prices over time. That is what Canada experienced starting in March 2022, when the Bank of Canada began hiking from a pandemic low of 0.25%, raising rates 10 times until the overnight rate peaked at 5.0% in July 2023. The Bank held at that level for nearly a year before reversing course. Since then, the Bank cut rates nine times between June 2024 and October 2025, bringing the overnight rate down to 2.25%. That cutting cycle has now paused, with the Bank holding the rate steady since October 2025.

Interest rates and rental properties: what landlords need to know

As interest rates stabilize, Canadian landlords will feel the impact in a variety of ways. Lower rates are drawing some buyers back into the market, which could soften rental demand at the margins in certain areas. However, the transition from renting to owning remains limited by ongoing affordability challenges, a soft labour market, and economic uncertainty tied to U.S. trade policy. In markets like Vancouver and Toronto, population contraction and reduced immigration have also eased rental demand somewhat. In other major centres, rental demand remains more resilient, supported by continued housing supply shortfalls and steady in-migration.

For landlords, the most direct effects of a stabilizing rate environment will show up in borrowing costs. Here is what to know about fixed and variable mortgage rates right now.

Mortgage rates

To properly explain how mortgage rates relate to inflation and changing interest rates, it’s first important to differentiate between fixed-rate and variable-rate mortgages. If you’re a landlord, you’ll likely already be familiar with these two terms and how they differ. Just in case though, let’s quickly look at the differences in each and how each will be affected by recent events.

Fixed-rate mortgages

Fixed-rate mortgages charge a set interest rate for the duration of the mortgage term, typically one to five years in Canada. At renewal, the rate is renegotiated at whatever the market offers at that time. For those currently within a fixed-rate term, monthly payments remain stable regardless of rate changes. This is one of the main reasons homeowners choose fixed-rate mortgages: they offer greater certainty during periods of rate volatility. However, landlords whose mortgages are coming up for renewal in 2026 should be prepared for higher payments, particularly those who locked in at pandemic-era rates as low as 1.5%–1.79%.

If you’re looking to purchase a property, be aware that five-year fixed rates rose to approximately 4.04%–4.29% in April 2026, as Government of Canada five-year bond yields climbed above 3% on geopolitical tensions and Canada-U.S. trade uncertainty. This happened independently of the Bank of Canada’s overnight rate: fixed mortgage rates follow the bond market, not the policy rate. When qualifying for a mortgage, you must also pass Canada’s mortgage stress test, which requires you to qualify at your contract rate plus 2%, or 5.25%, whichever is higher. At current rates of around 4.04%–4.29%, the operative qualifying rate is approximately 6.04%–6.29%.

Variable-rate mortgages

Variable-rate mortgages come in two forms in Canada: adjustable-rate mortgages, where the payment amount changes directly with the prime rate, and variable-rate mortgages, where the payment amount stays the same but the split between principal and interest shifts. Both types were affected by the rate-cutting cycle, with the prime rate falling from 7.20% to its current 4.45% between mid-2024 and October 2025. With the overnight rate on hold at 2.25%, variable-rate borrowers are seeing stable costs for now. However, the balance of risks has shifted: several major forecasters, including Scotiabank and Desjardins, now flag a possible rate hike in late 2026 if energy-driven inflation proves persistent, which would push prime-linked borrowing costs higher.

Credit card interest rates

For landlords who use credit cards to finance day-to-day expenses for their rental properties, the rate stabilization means credit costs are unlikely to rise further in the near term, provided the Bank of Canada holds its current position.

Savings accounts

With the rate-cutting cycle paused, the era of high savings account returns has likely peaked. Landlords who had been holding cash in high-interest savings accounts may find current yields less attractive, which could make this a reasonable time to revisit property investment or renovation plans.

How will stabilising interest rates affect rental prices?

Rent prices are fundamentally tied to inflation since they reflect a core part of the cost of living. As interest rates rose and then fell, landlords’ carrying costs shifted considerably. With the overnight rate holding at 2.25%, many landlords with variable-rate mortgages have seen some relief, though fixed-rate mortgages are slightly higher than earlier in 2026 due to bond market pressures.

Landlords who are re-listing units are navigating a more competitive market in many cities. Canada’s national purpose-built rental vacancy rate reached 3.1% in 2025, according to the Canada Mortgage and Housing Corporation (CMHC) 2025 Rental Market Report, up from 2.2% in 2024. This shift in supply may moderate how aggressively landlords raise rents going forward.

Landlords with existing tenants who choose to increase rent remain bound by provincial maximums. For 2026, Ontario’s rent increase guideline is 2.1%. In B.C., the 2026 maximum allowable increase is 2.3%. You can learn more in liv.rent’s guides on Ontario rent increases and B.C. rent increases.

Mortgage rates for rental properties

Those looking to purchase a property right now should know what to expect when it comes to mortgage rates. As of May 19, 2026, the best available rates according to Ratehub.ca are approximately 4.04% for a five-year fixed insured mortgage and 3.35% for a five-year variable insured mortgage nationally. Rates vary by lender, insured status, borrower profile, and province. Always consult the latest numbers before making any investment decision.

Mortgage rates are almost always higher for rental properties, since lenders prefer the security of owner-occupied residences. It’s always best to work with a knowledgeable mortgage broker to find the best rates for your needs, and don’t be afraid to shop around.

What’s next for Canada’s interest rates?

The Bank of Canada held its overnight rate at 2.25% on April 29, 2026, the fourth consecutive hold since the cutting cycle ended in October 2025. This decision came amid a complex backdrop: March inflation rose to 2.4% from 1.8% in February, driven by an energy price shock following geopolitical disruptions in the Middle East, and April inflation rose further to 2.8%. At the same time, Canada’s economy is dealing with weaker growth prospects, U.S. trade uncertainty, and a labour market that remains soft, with the unemployment rate in the 6.5%–7% range.

The Bank of Canada’s next announcement is scheduled for June 10, 2026. For the most current rate information, refer directly to the Bank of Canada’s policy interest rate page.

Here is the overnight rate timeline since late 2024, sourced from the Bank of Canada:

| Date | Rate |

|---|---|

| Dec 11, 2024 | 3.25% |

| Jan 29, 2025 | 3.00% |

| Mar 12, 2025 | 2.75% |

| Apr 16, 2025 | 2.75% (hold) |

| Jun 4, 2025 | 2.75% (hold) |

| Jul 30, 2025 | 2.75% (hold) |

| Sep 17, 2025 | 2.50% |

| Oct 29, 2025 | 2.25% |

| Dec 10, 2025 | 2.25% (hold) |

| Jan 28, 2026 | 2.25% (hold) |

| Mar 18, 2026 | 2.25% (hold) |

| Apr 29, 2026 | 2.25% (hold, most recent) |

Even with rates stabilizing at levels above the pandemic era, this situation isn’t all bad news for landlords. For those who already own a rental property, demand in the rental market remains strong. Persistently high home prices, elevated living costs, and population shifts continue to support rental demand across major Canadian markets.

FAQ: Interest rates, mortgage rates and rental property

Does a rental property have a higher mortgage rate?

Yes. Rental properties will almost always carry a higher mortgage rate, as they’re perceived as riskier by many lenders since the property won’t be owner-occupied.

What is the mortgage rate right now in Ontario?

As of May 19, 2026, the best available rate for a five-year fixed insured mortgage in Canada is approximately 4.04%, while the best five-year variable rate is around 3.35%, according to Ratehub.ca. These rates are available across Ontario. It’s always best to consult the latest numbers before making any investment decision, as rates change frequently.

What are current mortgage rates in Vancouver, BC?

As of May 19, 2026, the best available five-year fixed insured rate is approximately 4.04% and the best five-year variable rate is around 3.35% nationally, with these rates available in B.C. including Vancouver, according to Ratehub.ca. It’s always best to consult the latest numbers before making any investment decision.

Will mortgage rates go up in 2026?

Fixed rates have already risen somewhat in early 2026, driven by elevated bond yields tied to geopolitical and inflationary pressures. Variable rates remain steady, tied to the Bank of Canada’s paused overnight rate of 2.25%. Whether rates rise further depends largely on how inflation and global economic conditions evolve in the months ahead.

Why are interest rates higher for rental properties?

Mortgage rates are typically higher for rental properties since lenders see non-owner-occupied properties as a riskier investment.

How much higher is the interest rate on a rental property?

This depends on the situation and lender, but investors can generally expect to pay roughly 0.5%–0.6% more for a rental property mortgage compared to an owner-occupied residence.

What is a good ROI for a rental property?

A return on investment of 5%–10% or above is generally considered a good range for a rental property.

What is the current Bank of Canada overnight rate?

As of April 29, 2026, the Bank of Canada’s overnight rate is 2.25%. The next announcement is June 10, 2026.

How liv.rent helps landlords

In times of economic uncertainty, it’s more important than ever for landlords to rent their units quickly and safely in order to avoid vacancies and costly tenant-related issues. Using liv.rent, landlords can rent their unit in as little as seven days from listing to signing, with digital solutions for every step of the rental process. Finding qualified tenants is straightforward with marketing and rental management features like listing sharing to Facebook Marketplace, and tenant screening with the Trust Score — powered by Equifax credit reports. With this all-in-one rental platform, landlords and property managers can fill vacancies faster with verified tenants.

>> Recommended Reading: Landlord Success Story: How To Rent Out An Apartment In 10 Days

Resources for landlords

Here are some additional resources for landlords and investors looking to better understand the recent rise in interest rates and the resulting effects. For more tips and advice on how to rent out your property safely and quickly, be sure to check out liv.rent’s blog.

- Updated interest rates in Canada

- The Bank of Canada – Inflation in Canada

- Understanding the overnight rate

- Canadian Bankers’ Association – Understanding interest rates

For landlords whose mortgage payments have been affected by changing interest rates, it’s important to price your unit correctly in order to keep your rental property profitable. If you’re considering increasing rent, be aware that each province has a maximum allowable rent increase. For 2026, Ontario’s guideline is 2.1%. B.C.’s 2026 maximum is 2.3%.

Here are some additional resources related to rent prices and increases:

- Landlord Guide: How Much Should I Charge For Rent?

- Ontario – Residential rent increases

- B.C. – Rent Increases

Rethink The Way You Rent

Not on liv.rent yet? Experience the ease of digital applications & contracts, verified tenants & landlords, virtual tours and more – all on one platform. Sign up for free or download the app.

Subscribe to receive the latest tenant & landlord tips and get notified about changes in the Canadian rental market.

>> Stay up-to-date on the average rent in Vancouver, Toronto and Montreal: Rent Reports.

0 Comments